The American Financial Services Association and its members has long supported our nation’s military veterans, current servicemembers, and their families. It seems that with every passing year, the intent of Memorial Day becomes less apparent and important. And this year, with the pandemic, social distancing, and few of the usual events for us to gather as a nation to mark the solemnity of the day, it seems even more important to recall why Memorial Day is commemorated.

Memorial Day began as Decoration Day in the late 1860s to help reconcile the Confederate and Union veterans after the Civil War. As a result of the death-toll from that war the United States established national cemeteries, and in the wake of the war people across the country started tributes to fallen soldiers in the springtime, reciting prayers and decorating the graves of the fallen with flowers.

On May 30th 1868 Decoration Day was declared a federal holiday, and after World War I the holiday gained greater support and participation across the country, so much so that in 1968 the name of the holiday was changed to Memorial Day and moved to the last Monday of the month of May.

While it seems we as a nation have been spending a lot of time with our families and loved ones lately in a cycle of “holidays,” perhaps let us use this particular day to remind ourselves and our families, especially young people, about why and for whom we celebrate this day. Generations of men and women have served and defended our country because they believed America and its founding principles worthy of their sacrifice. We owe the fallen, as well as all veterans and their families, our deepest respect and gratitude, and we share that appreciation with all of them today.

We Call it Memorial Day for a Reason

May 25, 2020

The American Financial Services Association and its members has long supported our nation’s military veterans, current servicemembers, and their families. It seems that with every passing year, the intent of Memorial Day becomes… Read the rest

Counseling Solutions as Another Early Intervention Tool

May 22, 2020

Join us on Thursday, May 28 at 2:00 p.m. ET for Counseling Solutions as Another Early Intervention Tool, presented by Money Management International.

Money Management International (MMI) will provide an overview of currently available… Read the rest

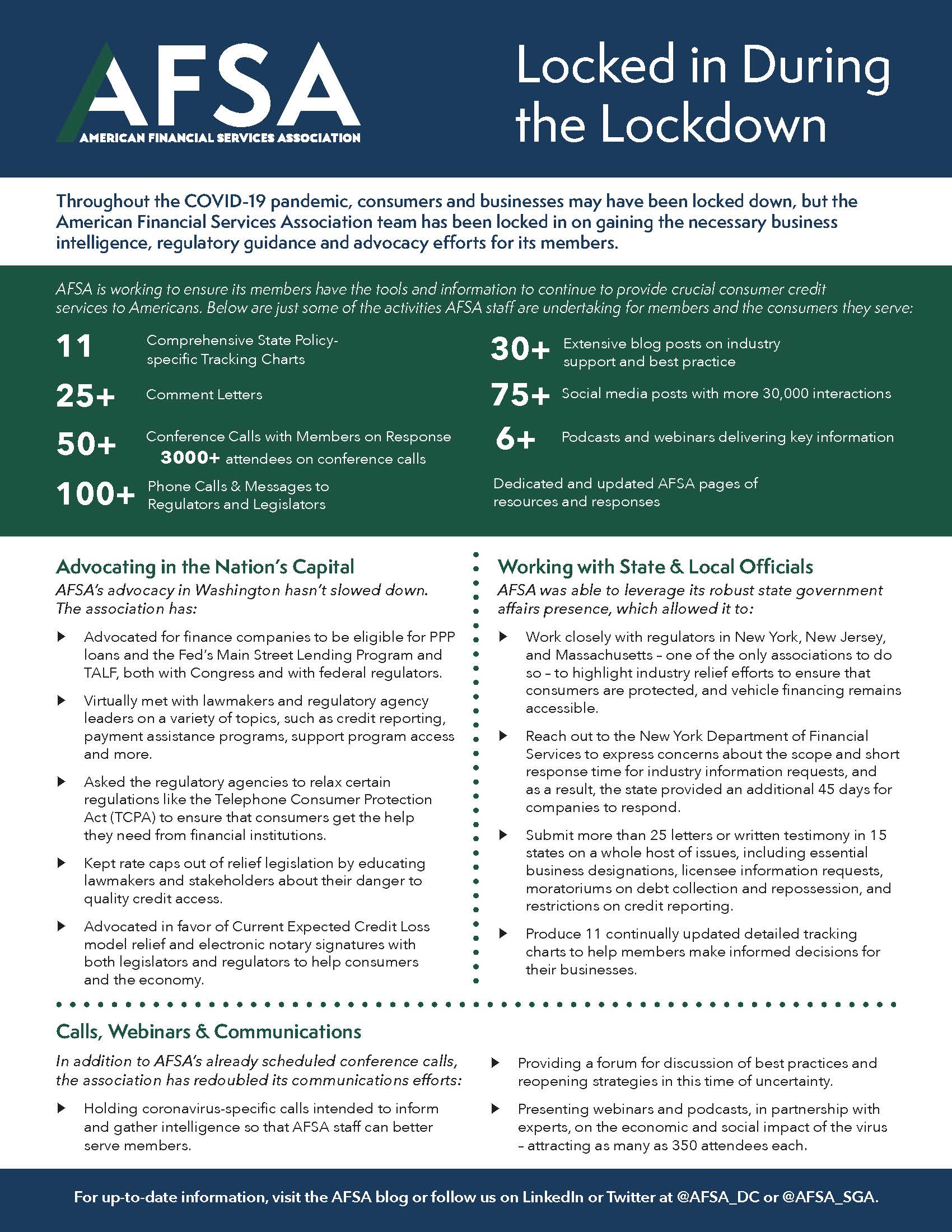

AFSA: Locked In During Lockdown

May 21, 2020

Installment Lending Meets Consumer Needs Now

May 21, 2020

The American Financial Services Association, the U.S. trade association for the consumer credit industry, has long supported increased options for consumers to access credit, including banks.

While regulators in Washington released… Read the rest

WEBINAR TOMORROW | Supporting Your Employees & Navigating Engagement

May 19, 2020

Join us on TOMORROW at 1:00 p.m. ET for Navigating Media and Consumer Engagement as We Emerge From the Pandemic presented by AFSA. The webinar will be conducted by Turbine Labs, which the association partners with to produce AFSA Daily Connect… Read the rest

Whether Lazy or Agenda Driven, Reporter Gets it Wrong

May 18, 2020

Recently, the Huffington Post published a story on the question of whether the Federal Reserve should expand one of its financing facilities, TALF, to include additional auto asset-backed securities (ABS) and consumer installment loan… Read the rest

AFSA Submits Comment Letter to FCC on Robocall Blocking

May 18, 2020

On May 15, AFSA submitted a letter to the FCC requesting that the agency begin a rulemaking as soon as possible to ensure that all robocall blocking services include transparency and effective redress options for both consumers and callers.… Read the rest

Navigating Media and Consumer Engagement as We Emerge From the Pandemic

May 15, 2020

Join us on May 20 at 2:00 p.m. ET for Navigating Media and Consumer Engagement as We Emerge From the Pandemic presented by AFSA. The webinar will be conducted by Turbine Labs, which the association partners with to produce AFSA Daily Connect… Read the rest

Announcing the New AFSA AdvantEDGE Affinity Program

May 15, 2020

As the American economy begins to slowly reopen, the American Financial Services Association is pleased to announce another way to help members manage their business and defray some of the day-to-day costs of supporting the communities … Read the rest

SBA Updates Loan Guidelines

May 14, 2020

The Small Business Administration (SBA) in the past 48 hours has updated their guidelines for both the review and return of Paycheck Protection Program (PPP) loans in two FAQs.

FAQ 46 states that the SBA will consider any borrower that received… Read the rest