New AFSA Survey: Lenders Saw Weak Q1 2024, But Improvement Expected

Results from AFSA’s new Consumer Credit Conditions Index (C3) reflect the challenges faced by lenders and borrowers in today’s volatile economic and regulatory climate.

This view from lenders is the result of a first-of-its kind survey of AFSA’s membership of providers of consumer credit in the form of mortgages, vehicle financing, personal installment loans, credit cards, and other products. Moving forward, participants will provide their views each financial quarter on several key business indicators, including how they see consumer lending evolving in the coming months.

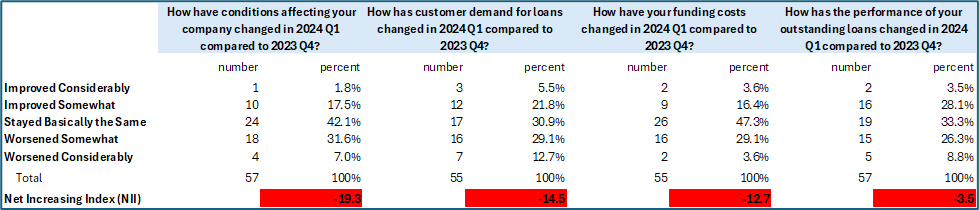

On balance, conditions facing consumer lenders deteriorated in the first quarter of 2024, compared to the fourth quarter of 2023. Twice as many lenders said that business conditions worsened in Q1 2024 compared to Q4 2023 (38.6 percent) as said they improved (19.3 percent). The “Net Improving Index (NII),” the percentage of those reporting improving conditions minus the percentage reporting worsening conditions, was -19.3. Conditions were basically unchanged in Q1, according to 42.1 percent of survey participants.

Participants were asked if customer demand for loans, funding costs, and performance of outstanding loans improved, worsened, or stayed the same in the first quarter of 2024 compared to the fourth quarter of 2023. In every case, the share of participants reporting the indicator worsened exceeded the share reporting it improved. NIIs for loan demand, funding costs, and loan performance, respectively, measured -14.5, -12.7, and -3.5.

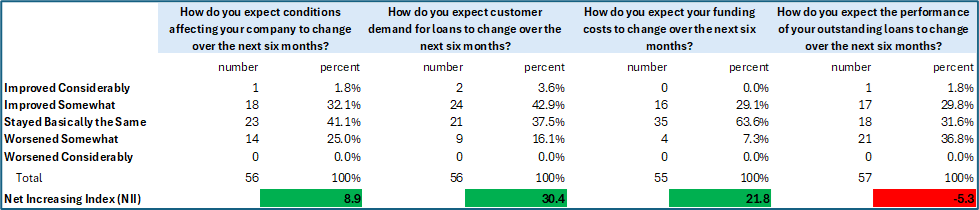

Lenders expressed some greater degree of optimism, though, regarding the business outlook six months hence.

When asked how they expect conditions affecting their company to change over the next six months, 33.9 percent said they expect some degree of improvement compared to 25 percent expecting conditions to worsen, for an NII of +8.9. The NII for the six-month loan demand outlook measured +30.4, while the NII for the six-month funding cost outlook was +21.8. However, survey respondents remained pessimistic on balance (NII of -5.3) regarding the six-month outlook for the performance of outstanding loans.

Additional detailed results, as well as a description of the survey methodology can be found here.

April 18th, 2024