Credit Balances Hit Record High

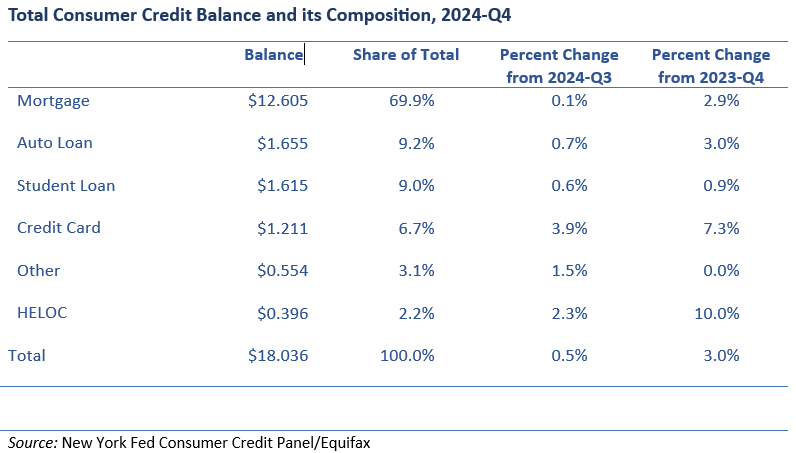

In the fourth quarter of 2024 consumer credit balances topped $18 trillion for the first time, according to the Federal Reserve Bank of New York’s latest Quarterly Report on Household Debt and Credit, which draws on data from the bank’s Consumer Credit Panel/Equifax. That was an increase of $93 billion, or 0.5 percent, from the third quarter of 2024 and an increase of $530 billion, or 3 percent, from the fourth quarter of 2023.

Home mortgages made up the largest share of consumer credit balances at the end of 2024. The more than $12.6 trillion in outstanding mortgage credit accounted for nearly 70 percent of the total. Home equity lines of credit (HELOCS), also secured by residential real estate, comprised another 2.2 percent of the total.

Auto and student loans had the largest outstanding balances among non-residential types of consumer credit, at $1.7 and $1.6 trillion respectively. Each accounted for approximately 9 percent of the total. Credit card balances amounted to $1.2 trillion at the end of 2024, 6.7 percent of the total. Balances on “other” loans, a category including personal loans and retail finance, measured just over $0.5 trillion, 3.1 percent of the total.

Over the course of 2024, growth in balances on revolving loan products such as HELOC’s (up 10 percent Q4/Q4) and credit cards (up 7.3 percent Q4/Q4) outpaced overall consumer credit growth. Auto loan balances increased 3 percent Q4/Q4, matching the overall pace of growth, with mortgage balances slightly slower at 2.9 percent Q4/Q4. “other” loans balances were nearly unchanged in 2024.

These figures are broadly consistent with the Federal Reserve Board of Governors’ monthly G.19 Consumer Credit data release. Based on data from lender surveys rather than consumer credit reports and limited to loans not secured by residential real estate, the December G.19 estimated non-housing consumer credit outstanding at $5.15 trillion in December, 2.4 percent higher than at the end of 2023. Similarly, the G.19 shows revolving balances growing at a faster rate than nonrevolving balances in late 2024.

Some context: although credit balances are at a record high so, too, are household incomes. The ratio of outstanding consumer credit balances reported by the New York Fed to disposable personal income fell to its lowest in three-and-a-half years in the fourth quarter of 2024 and was at the low end of its range over the 22-year period for which this data is available.

The New York Fed’s report also provides an abundance of data on consumer loan originations and loan performance, as well as breakdowns by age cohort and geography. AFSA’s next bi-weekly Economy Matters newsletter on February 25 will dive deeper into this data.

February 14th, 2025