Overview: AFSA’s C3 Index

This report presents the results of a first-of-its kind survey of leading providers of mortgages, vehicle financing, personal installment loans, credit cards, and other consumer products. Participants provide their views on several key business indicators, including how they see consumer lending evolving in the coming months.

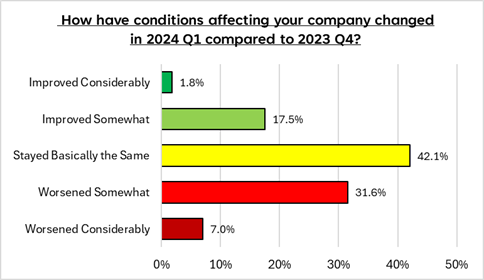

The survey’s results show conditions facing consumer lenders deteriorated on balance in the first quarter of 2024, compared to the fourth quarter of 2023:

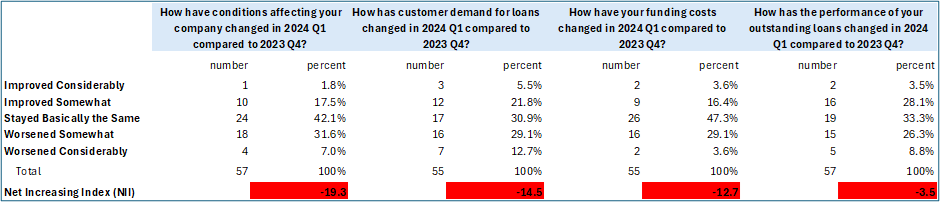

- Twice as many lenders said that business conditions worsened in Q1 (38.6 percent) as said they improved (19.3 percent). The “Net Improving Index (NII),” the percentage of those reporting improving conditions minus the percentage reporting worsening conditions, was -19.3. Conditions were basically unchanged in Q1, according to 42.1 percent of survey participants.

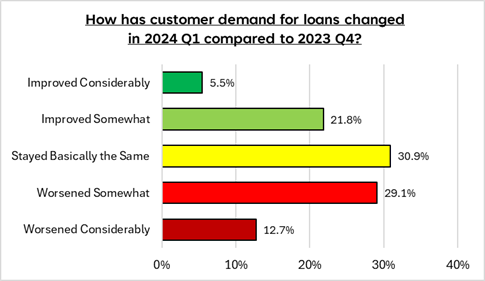

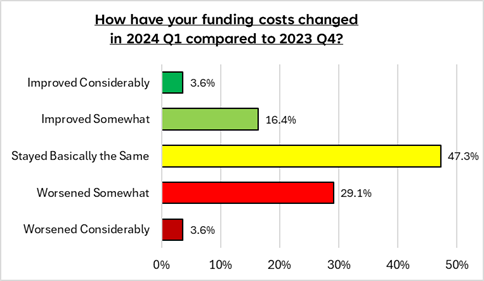

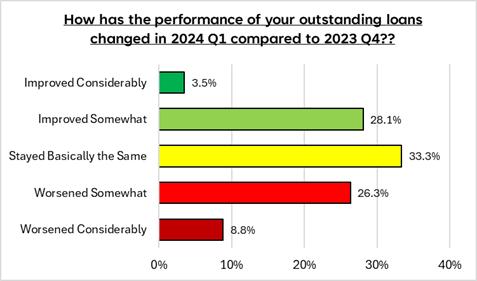

- Participants were asked if customer demand for loans, funding costs, and performance of outstanding loans improved, worsened, or stayed the same in the first quarter of 2024 compared to the fourth quarter of 2023. In every case, the share of participants reporting the indicator worsened exceeded the share reporting it improved. NIIs for loan demand, funding costs, and loan performance, respectively, measured -14.5, -12.7, and -3.5.

Lenders, however, expressed a greater degree of optimism regarding the business outlook six months hence.

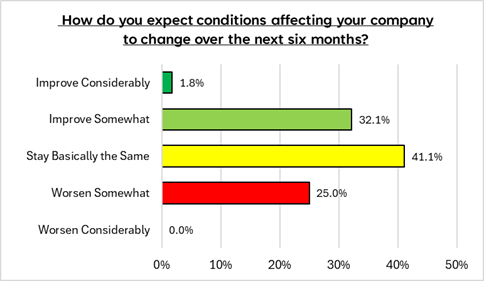

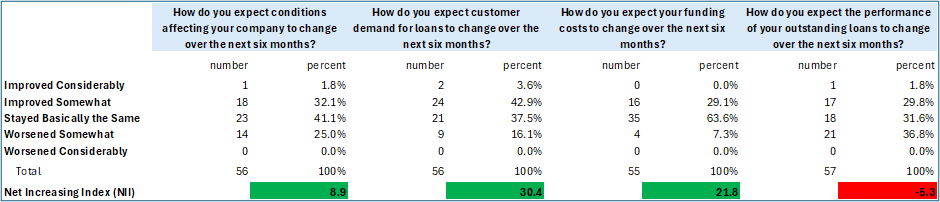

- When asked how they expect conditions affecting their company to change over the next six months, 33.9 percent said they expect some degree of improvement compared to 25 percent expecting conditions to worsen, for an NII of +8.9.

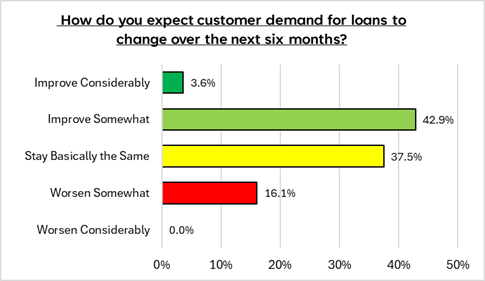

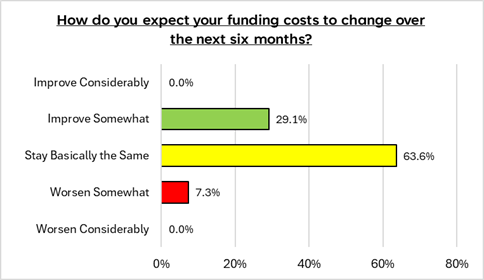

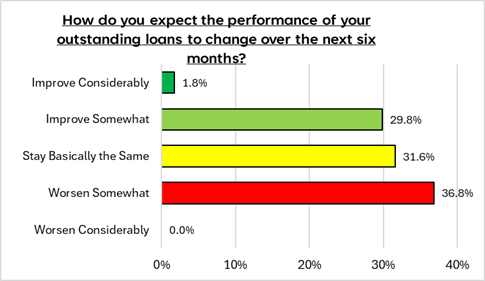

- The NII for the six-month loan demand outlook measured +30.4, while the NII for the six-month funding cost outlook was +21.8. However, survey respondents remained pessimistic on balance (NII of -5.3) regarding the six-month outlook for the performance of outstanding loans.

The following charts summarize survey results for the full consumer credit sector. Additional detailed results, as well as a description of the survey methodology are provided in appendices.

Current Conditions

Overall Conditions: NII -19.3

Customer Demand: NII -14.5

Funding Costs: NII -12.7

Loan Performance: -3.5

Expected Conditions

Overall Conditions: NII +8.9

Customer Demand: NII +30.4

Funding Costs: NII +21.8

Loan Performance: NII -5.3

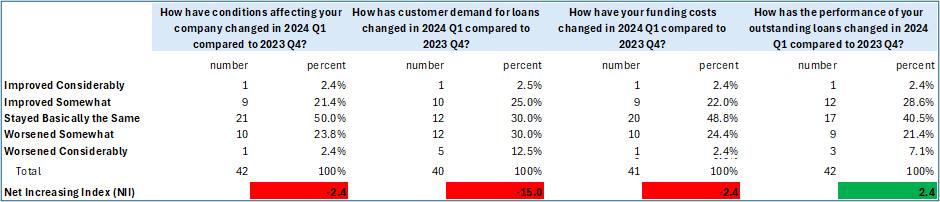

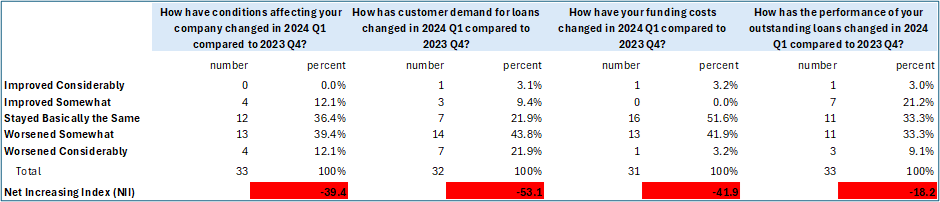

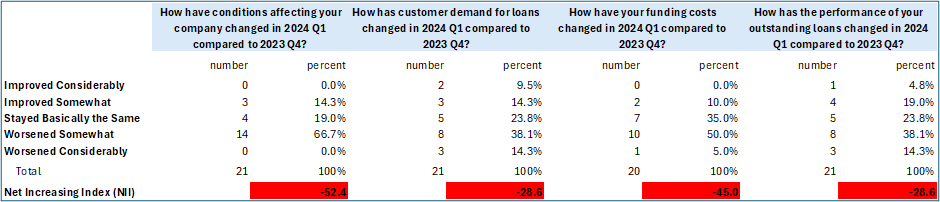

Appendix 1: Data Tables

Current Conditions

All Lenders

Vehicle Financing

Personal Installment Loans

Other

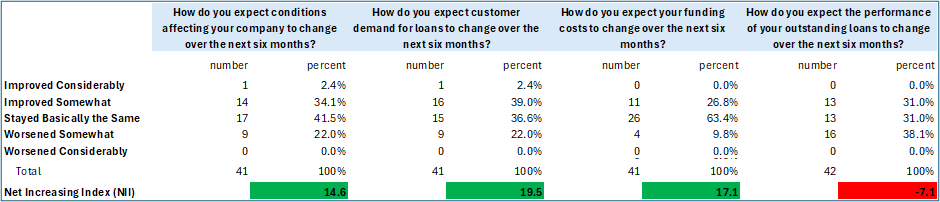

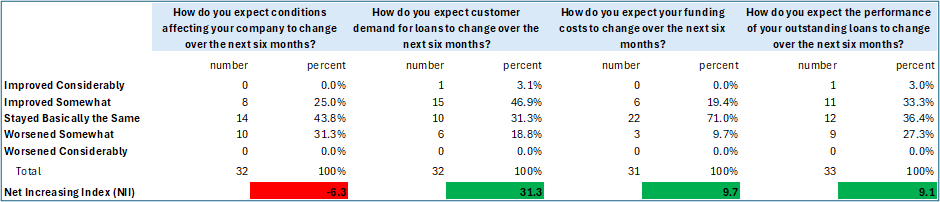

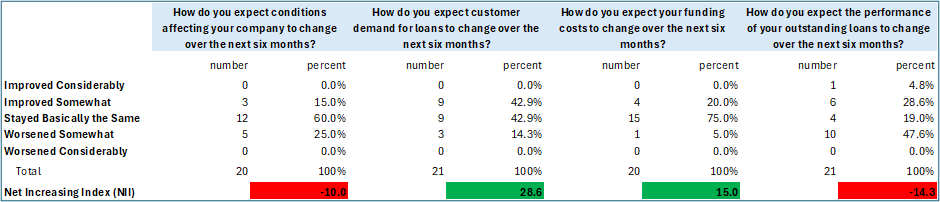

Expected Conditions

All Lenders

Vehicle Financing

Personal Installment Loans

Other

Appendix 2: Methodology

The results presented in this report are derived from a survey of senior executives of 175 AFSA finance company members. The survey was conducted between March 27 and April 8, 2024. Fifty-seven (57) participants responded to at least one question. Response counts for individual questions are shown in the accompanying charts and data tables.

The survey consisted of the following questions:

- Considering all factors, how have conditions affecting your company changed in the first quarter of 2024 compared to the fourth quarter of 2023?

- How has customer demand for loans changed in the first quarter of 2024 compared to the fourth quarter of 2023?

- How have your funding costs changed in the first quarter of 2024 compared to the fourth quarter of 2023?

- How has the performance of your outstanding loans changed in the first quarter of 2024 compared to the fourth quarter of 2023?

- Considering all factors, how do you expect conditions affecting your company to change over the next six months?

- How do you expect customer demand for loans to change over the next six months?

- How do you expect your funding costs to change over the next six months?

- How do you expect the performance of your outstanding loans to change over the next six months?

For questions regarding current conditions, participants were asked if conditions relative to the previous quarter “improved considerably,” “improved somewhat,” “stayed basically the same,” “worsened somewhat,” or “worsened considerably.” For questions regarding expected conditions, participants were asked if conditions over the next six months would “improve considerably,” “improved somewhat,” “stay basically the same,” “worsen somewhat,” or “worsen considerably.”

Index Calculation. The Net Improving Index (NII) for current conditions questions is calculated as the percentage of participants reporting conditions “improved considerably” or “improved somewhat” minus the percentage reporting conditions “worsened somewhat” or “worsened considerably.”

The NII for future conditions questions is calculated as the percentage of participants reporting they expect conditions to “improve considerably” or “improve somewhat” minus the percentage reporting they expect conditions to “worsen somewhat” or “worsen considerably.”

Breakdown by Type of Credit Offered. Participants were asked to indicate the types of consumer credit provided by their company: “credit cards,” “personal installment loans,” “vehicle financing, “sales financing,” “student loans,” “mortgages/ home equity loans,” and “other.” They were not, however, asked to provide separate responses for each type of credit offered, only a consolidated evaluation of conditions affecting their company as a whole. If a company provides both personal installment loans and vehicle financing, for example, its responses are included in the compilation of results for “all lenders,” as well as for “vehicle financing” and “personal installment loans.” Thus, the number of responses summed across credit types will not necessarily equal the total number of responses for a given question.

The number of responses indicating their company offered credit cards, sales financing, student loans, mortgages/home equity loans, and other types of credit were insufficient to report separately. These were aggregated and reported as a single “other” category.

April 18th, 2024

Recent Posts

- This Thursday | AFSA Webinar | Usage-Based Models: Reinventing Auto & Equipment Finance

- Industry Expertise | Four Ways Lenders Can Get Paid Faster

- Kentucky’s U-Drive-It Program

- CFPB Steps Away from BNPL and Toward Military Issues

- Industry Expertise | Vehicle-finance fraud is a $9 billion problem. Here’s how to combat it.