How Automated Credit Dispute Handling Can Reduce Costs by 90%

AFSA’s Industry Expertise allows Business Partners to provide thought leadership and best practices information directly with AFSA member companies. For more information about taking part, contact Dan Bucherer.

By Badri Sridhar, Managing Director, FTI Consulting; David Holland, Senior Director, FTI Consulting; and Evan Ruschell, Director, FTI Consulting

The following article summarizes takeaways from a webinar presented for AFSA members on automated credit dispute handling. Click here to view the full webinar on YouTube.

Since 2020, there has been a significant increase in the number of credit disputes while financial institutions continue to feel the strain of hiring and retaining the staff that process them. These clashing trends have led institutions to seek more automation in their disputes handling processes. This article will discuss:

- Direct vs. Indirect Disputes

- Best Practices in Automated Credit Disputes Handling

- How Automated Credit Dispute Handling Can Increase Accuracy and Provide Cost Benefits

Direct vs. Indirect Disputes

A key cornerstone of the consumer credit reporting ecosystem is the expectation of accuracy and integrity of information provided from data furnishers (e.g., financial institutions) to Consumer Reporting Agencies (CRAs). However, consumers can actively participate in the system by disputing information they believe to be inaccurate, via direct and indirect disputes. Regardless of how the dispute originates, all disputes should be responded to within the statutory timeframes (i.e., 30 to 45 days after receipt), after a reasonable investigation is performed.

With direct disputes, consumers might have multiple channels (e.g., phone, email, mail, fax) to contact the furnisher. Indirect disputes are sent from the customer to the CRA, who then reviews and determines if they need to reach out to the furnisher for clarification. If the CRA determines that the furnisher is required to investigate, the dispute is sent to the furnisher via the e-OSCAR platform through what is called an Automated Credit Dispute Verification (ACDV). e-OSCAR is an automated credit dispute system that allows for consistency in data formats between furnishers and CRAs and is the web portal through which furnishers respond to disputes.

As indirect disputes are only received through the e-OSCAR portal, it is a more consistent process that allows for more reporting analytics on the file and, as discussed below, increased possibilities for automation.

Best Practices in Automated Disputes Handling – High-Level Process and Overview

Advancements in technology, such as the new e-OSCAR API, unlock new opportunities to use software to increase accuracy and automate time-consuming steps in the dispute resolution process. Consistency in indirect disputes also makes the process suitable for automated tooling.

Indirect disputes have multiple consistencies across all disputes, including:

- They are received through the e-OSCAR portal;

- They are assigned a code based on what the customer is disputing (allowing the tool to easily identify the core issue);

- Supporting documentation is provided through e-OSCAR (i.e., furnishers do not need to reach out to customers to request supplemental documentation); and,

- Furnishers respond to disputes through e-OSCAR.

These consistencies allow for streamlining and automation that can drive efficiencies and increase accuracy. While the nature of indirect disputes allows for a more streamlined approach, direct disputes can also be automated to some extent.

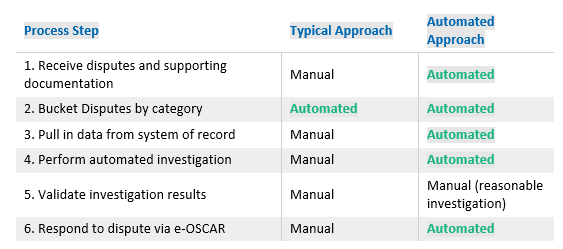

FTI Consulting has developed a prototype for an automated tool to handle all fields associated with disputes which follows this high-level process:

In a typical dispute handling process, all steps are performed manually with the exception of Step 2. In the automated approach outlined above, all steps are automated with the exception of Step 5, where some manual validation is expected for a reasonable investigation. By automating the other steps, institutions save time, reduce costs, and improve accuracy.

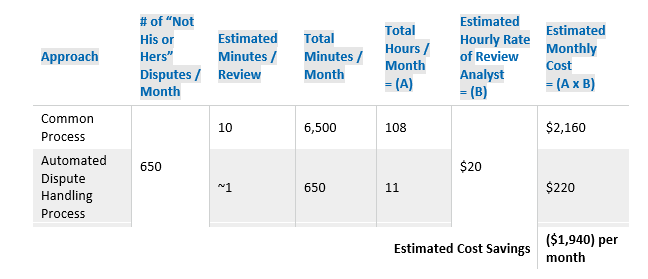

When using automation to streamline the dispute review process, we estimate it would conservatively take one minute for validation to occur, or 10 percent of the manual processing time. This results in a 90% reduction in costs that can be redirected toward robust analysis of more complicated disputes and/or priority initiatives.

Conclusion

Today, financial institutions face a difficult confluence of an increased volume of disputes with simultaneous difficulties in hiring and retaining staff to process them. Having a rigorous automated review process that integrates information from multiple systems of record is imperative for institutions as it allows for an efficient reasonable investigation, reduces dispute handling costs and labor requirements, and ultimately results in a more accurate disputes process for the consumer that can withstand regulatory scrutiny.

For more information on how automated credit dispute handling can benefit your organization, please do not hesitate to contact us:

- Badri Sridhar, Managing Director – Badri.Sridhar@fticonsulting.com

- David Holland, Senior Director – David.Holland@fticonsulting.com

- Evan Ruschell, Director – Evan.Ruschell@fticonsulting.com

January 16th, 2023

Get The News You Need

Sign up for our daily newsletter to receive all the most important industry news and updates every weekday morning.

Recent Posts

- New Guidance on Non-Work Authorized Borrowers

- CFPB’s Semi-Annual Report

- 🚨THIS THURSDAY | AFSA Webinar | Beyond the Paperwork: Stopping Asset Finance Fraud with Identity Intelligence and Intelligent Decisioning

- AFSA Shares Debt Collection Rules FAQs

- Chopra CFPB vs. Current Bureau