The BBB Must be Better on Consumer Credit

The Better Business Bureau, International (BBB) has released a report on predatory payday and cash-advance lenders and debt collection scams. The report generally raises three issues. First, the BBB says its “scam tracker” identified 750 annual consumer complaints since 2020 regarding payday and cash advance scams; the report also cites some general data from the CFPB and the FTC.

Second, the BBB fails to differentiate among the diverse options most consumers have for small dollar loans. This failure creates confusion for consumers and may lead them to believe they have limited options to meet their financial needs. In pulling this report together, however, the BBB provides no real research of its own, falling back on rightly troubling customer anecdotes with predatory lenders.

Third, the BBB also endorses a national 36% rate cap as the panacea for the payday problem, revealing not only the lack of rigor of the BBB report, but also the lack of due diligence the BBB undertook to come to that policy endorsement. Let’s address each of these issues.

On the first point, AFSA supports efforts from organizations like the BBB to protect customers from predatory lenders, as well as debt collection and credit repair scams of all stripes. We do so because we care about the customers we serve and the communities we live and work in. AFSA members offer Traditional Installment Loans, (TILs) which are regulated at the state and federal levels, underwritten, with an evaluation of a borrower’s ability to repay; transparent, with easy-to-understand terms; a fixed rate with equal monthly payments; and a defined payoff date that averages between 12 to 18 months. There are no hidden fees, balloon payments or prepayment penalties. Further, repayment histories are reported to credit bureaus, which give consumers the opportunity to build or strengthen their credit history.

The hallmarks of TILs, which have been used by tens of millions of U.S. consumers for more than a century, are important differentiators from payday, advanced pay and other loan products. Beyond BBB’s seeming lack of awareness on these points, there are other issues with the report that mislead consumers.

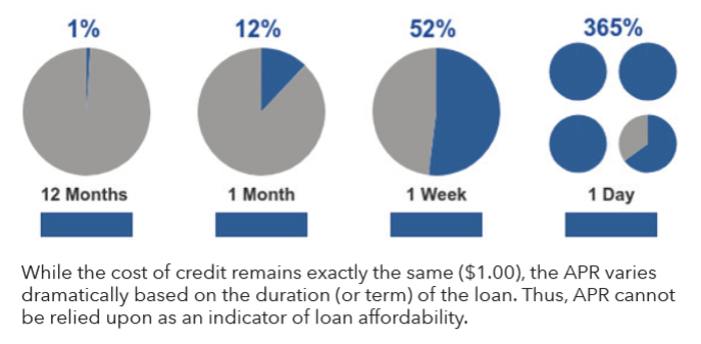

On the second point, the BBB appears to have a fundamental misunderstanding not only of the industry, but how Annual Percentage Rates (APRs) and small dollar lending work. APRs are a function of time, rather than a measure of the cost of a loan. For example, say you borrow $100 today and are charged $1 in interest. If you repay the loan in one year, the APR is 1%. Repay it in a month, the rate is 12%. If you repay the loan tomorrow, the APR is 365%. Same dollar in interest, vastly different APRs, as this chart reflects:

In the case of TILs, the APR is not an accurate reflection of the affordability and soundness of the loan. Rather, the length and monthly amount owed provides consumers with a clearer view on the loan.

Lastly, let’s look at the BBB’s endorsement of a federal 36% rate cap. The BBB cites the seeming success of Illinois’ 36% rate cap and that of the Military Lending Act, which sets a 36% APR cap for many loans made to active military servicemembers. On the contrary, both caps hurt the very borrowers they are intended to protect. Highlighting them reveals the BBB’s fundamental lack of understanding on the issues.

There is a great deal of data that shows rate caps eliminate access to small loans. More specifically, a 36% rate cap eliminates loans below approximately $2500. Such caps actually hinder consumer choices, particularly for those with nonprime credit scores (credit score below 670) or those with little or no credit history.

In the case of Illinois, an independent study found that at least 36% of consumers in that state – many with less than stellar credit scores or little to no credit history – no longer qualify for any form of consumer credit.

Why? Because most legitimate lenders cannot afford to offer a small dollar loan capped at 36% without taking a loss due to underwriting and regulatory costs. These require a minimum loan amount of about $2500, when most consumers are looking for considerably smaller loans.

This has been confirmed in the National Commission on Consumer Finance study. The Consumer Financial Protection Bureau Task Force on Federal Consumer Financial Law report confirmed it. A Federal Reserve study on interest rate caps confirmed it.

Earlier this year, the Congressional Black Caucus Foundation annual report highlighted the importance of maintaining a financial marketplace that allows access to small-dollar credit. Most notably, the report cited “proposals to protect consumers from predatory practices through a 36% rate cap would cause more harm than help by limiting consumer access to credit.” The Financial Health Network similarly found that rate caps reduce consumers’ credit options.

Moving on from Illinois, let’s look at the BBB’s misplaced faith in the Military Lending Act (MLA). Independent surveys in the past several years have highlighted the MLA’s 36% interest rate cap harm on military service borrowers. The surveys reveal the MLA restricts access to traditional installment loans, forcing servicemembers to borrow larger amounts than they need or want, with higher costs and longer repayment periods, despite having a lower APR. That is, if they even qualify for the larger loan amount.

The National Foundation for Credit Counseling (NFCC) 2020 financial readiness survey of servicemembers, reported, “Over three-quarters of active duty servicemembers (78 percent) have taken out a loan in the past year. … However, the type of loan has changed dramatically. This year, 31 percent of active duty servicemembers have taken out a cash advance or payday loan, compared to only 13 percent in 2019. This represents an even more dramatic shift since 2014, when just six percent of active duty servicemembers reported taking out such loans.”

The NFCC survey indicated that servicemembers and their families were more than twice as likely to take out a cash advance or payday loan in 2020 than in 2019. What is most troubling about this survey result is that under the MLA, legitimate lenders are barred from making such loans, and servicemembers are instead admitting to turning to payday lenders, the very types of loans the MLA was intended to hinder.

Which raises another point in the BBB’s support for the MLA and the 36% rate cap. While there is plenty of evidence that active military servicemembers and their families are accessing predatory lenders, the Department of Defense has not released any verifiable data – let alone any data whatsoever – regarding the MLA and whether it is assisting active military servicemembers and their families or that the MLA is being appropriately and widely enforced. This, despite the fact that the Consumer Financial Protection Bureau has taken enforcement actions against predatory lenders for violating the MLA.

AFSA is happy to work with such organizations as the BBB, both in assisting consumers but also in addressing appropriate consumers protections against predatory lenders. But always, in protecting consumers we must ensure that policies likewise do not hinder their ability to access the forms of credit that best meet their financial needs.

September 27th, 2022

Get The News You Need

Sign up for our daily newsletter to receive all the most important industry news and updates every weekday morning.

Recent Posts

- Defending Credit in Oregon

- THIS THURSDAY | AFSA Webinar | Why AI Implementations Fail, and How Asset Finance Lenders Can Get It Right

- On Brian Johnson’s Nomination to Lead the CFPB

- June White Paper | Consumer Complaints

- NY Fed on Rate Caps