The WSJ Did Not Try to Get it Right….We Set the Record Straight

A news article published this week in The Wall Street Journal claims that U.S. consumers in the subprime credit tier are beginning to fall behind on their auto loans. While the article presents data, it doesn’t explain the data; important measurements and context are absent. The result is a deceptive, inaccurate article.

A number of our member companies, many significant national players in the marketplace, are reporting late-stage delinquency rates being relatively flat quarter to quarter in this fiscal year, and down year over year. Similarly, they saw higher payment rates across all FICO tiers in Q4 2020 year over year, including deferred accounts. Obviously, a number of other considerations come into play, but generally our member data presents a very different picture than what The Journal chose to present.

AFSA members who lend to subprime borrowers report that delinquencies overall are at record lows. Their data shows that subprime delinquencies for borrowers who were more than 60 days past due range from less than a percent to around 6%.

The WSJ article, on the other hand, is reporting that 10.9% of subprime auto borrowers were more than 60 days past due in February, up from January 2021 and an increase from February 2020. The article also says that more than 9% of subprime auto borrowers were more than 60 days past due in the fourth quarter, the highest quarterly figure in data going back to 2005. Here’s what the article doesn’t explain:

- Those delinquency percentages are a snapshot in time. They are the answer to a simple equation: total number of active subprime auto consumers delinquent (60+ days past due) divided by total number of active subprime auto consumers. Because the number of active subprime auto consumers is down, the delinquency rates look higher. Given the reduction in total number of active subprime auto consumers in 2021, it’s likely the increase in this delinquency rate does not necessarily reflect an increase in delinquent subprime auto consumers.

- AFSA members track the performance of their loans over time. The standard industry practice is to use vintage analysis to monitor for performance and risk. Furthermore, aggregate delinquency rates do not capture each lender’s unique portfolio characteristics that affect their delinquency rates. Using this method of analysis AFSA members’ internal data shows that delinquency rates are actually at historic lows.

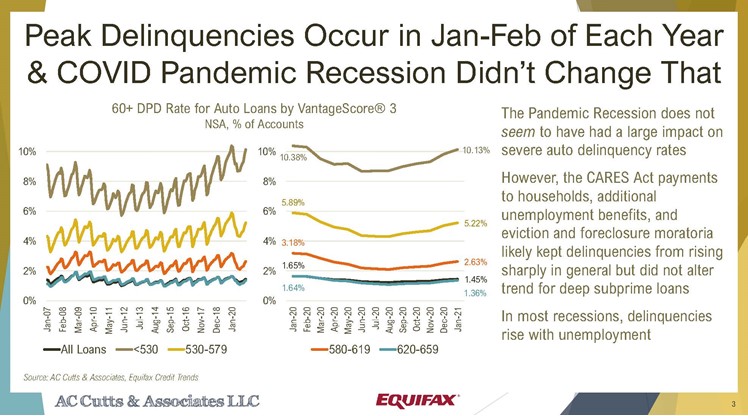

- Delinquencies are always higher in January and February due to cyclical factors, such as holiday spending. This makes the two months The Journal used for its article inappropriate for comparison to any other part of the year. Delinquencies consistently tend to return to normal in March, and early data is showing that delinquencies dropped substantially in March compared to February.

- TransUnion’s definition of subprime borrowers includes borrowers with credit scores from 300 – 600. However, if you separate out subprime and deep subprime, you get a different story, as the slide below demonstrates.

Fitch also found that subprime auto delinquencies aren’t going above 6% and dropped in the beginning of this year.

According to recent KBRA data, the 60 day+ delinquency rates among non-prime borrowers has fallen to just over six percent, a far cry from the nine percent stated by The Journal. The Journal’s cherry-picking of data is compounded by additional facts the reporters chose to either ignore or not disclose: the dramatic set of weather events that played out in late January, especially in Texas.

We doubt that ignoring all of this data was unintended. Why? Because it undercuts the narrative the reporters wished to pursue and reveals a very different story from the one The Journal ran.

So why are delinquency rates at historically low levels? We believe it is largely due to the industry response to the coronavirus pandemic. A year ago, it was anticipated that consumers financially disrupted by the pandemic would need help, particularly those who lost jobs or saw their hourly wages significantly affected by the dramatic economic downturn.

Creditors responded the way they always do when customers face hardships like hurricanes, earthquakes, etc. They offered loss mitigation tools like they always have, but due to the nationwide scope and sudden onset of the pandemic, the effort was even more meaningful. They took this action to help consumers stay in their vehicles and continue to have a trusting relationship with lenders. And of course, the stimulus checks and unemployment money helped too.

Unfortunately, playing fast and loose with the numbers is not new for The Journal. In 2019 its reporters tracked several other stories related to auto sales and financing, using the same formula: find a couple of outrageous anecdotes and then selectively pick data points to add the patina of a “national trend.” But cherry-picked anecdotes and data do not a trend make.

AFSA member companies have always been there to support consumers through trying times, from a job loss to life-altering natural disasters. It is one of the great differentiators between traditional installment lenders and auto-finance lenders and less reputable payday or vehicle title lenders. It is a good story to tell. We are happy to share it and would hope fact-based reporters would find it compelling. This incident highlights another important component to our industry.

Trust is a big part of the relationship between a lender and a customer. Trust is earned. It is also diminished … in this case when reporters choose to not do basic due diligence to get the facts right.

April 7th, 2021

Get The News You Need

Sign up for our daily newsletter to receive all the most important industry news and updates every weekday morning.

Recent Posts

- Industry Expertise | The Exposure Gap Your Bank Partnership Agreement Just Created

- AFSA Connects on the West Coast

- AFSA Testifies on Capitol Hill

- Colorado Automated Decision-Making Technology

- New Guidance on Non-Work Authorized Borrowers