Fed: Credit Balances on the Rise

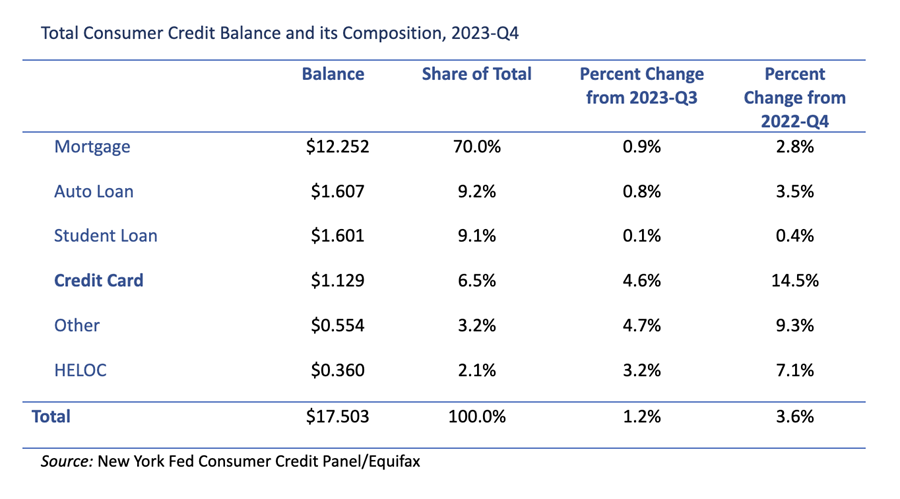

Consumer credit balances reached a record $17.5 trillion in the fourth quarter of 2023, according to the Federal Reserve Bank of New York’s latest Quarterly Report on Household Debt and Credit, which draws on data from the bank’s Consumer Credit Panel and Equifax. That was an increase of $212 billion, or 1.2 percent, from the third quarter and an increase of $604 billion, or 3.6 percent, from the fourth quarter of 2022.

Home mortgages, including home equity installment loans, made up by far the largest share of consumer credit balances at the end of 2023, as shown in the table below. Credit cards and “other” loans, a category including personal loans and retail finance, saw the fastest growth in balances both on a quarter-over-quarter basis and a year-over-year basis.

Meanwhile, the Federal Reserve Board of Governors’ monthly Consumer Credit data release, based on data from lender surveys, estimated outstanding non-housing consumer credit at just over $5 trillion in December, an increase of $32 billion over the last three months of 2023. Revolving credit balances, mostly on credit cards, grew at more than twice the volume of nonrevolving credit—$22 billion compared to $10 billion.

The New York Fed report also provides an abundance of data on loan performance. Although, the share of total delinquent balances remained low in the fourth quarter by historic standards, it did increase for a second straight quarter and at 3.1 percent was at its highest since the first quarter of 2021. As a general matter, mortgage and home equity lines continue to perform well, with credit cards, auto loans and “other” loans showing various degrees of stress. Student loan delinquencies, meanwhile, will not be reported to credit bureaus until the end of the year.

Approximately 1.7 percent of total balances were 90 days or more delinquent. Credit cards had the highest share of balances among major loan types in this status. And, at 9.7 percent, their share was at its highest since the first quarter of 2021. “Other” loans were next, with 7.9 percent of balances 90 or more days delinquent. This matched the previous quarter’s share as the highest share since 2015. Some 4.2 percent of auto loan balances were 90 days or more delinquent, up from 3.9 percent in the previous quarter and their highest since second quarter of 2021.

Rates of transition into 30-day delinquency continued on the rise in the fourth quarter, with 3.6 percent of total balances becoming delinquent. This is the highest rate in three and a half years. More than 8.5 percent of credit card balances became delinquent in the fourth quarter, up from 8.0 percent in the third. The fourth quarter transition rate for credit card balances was the highest in more than 12 years. Nearly 7.7 percent of auto loan balances transitioned to delinquency in the fourth quarter, the highest since 2010. “Other” loan balances transitioned to delinquency at a 7.5 percent rate in the fourth quarter, the highest since 2012.

Overall rates of transition into severe delinquency (90-days or more) remained relatively subdued, with 1.4 percent of total balances becoming delinquent in the fourth quarter. That was the highest rate since mid-2020, but again still low by historic standards. Nearly 6.4 percent of credit card balances transitioned into severe delinquency in the fourth quarter, the highest since 2011, and up from 5.8 percent in the third. “Other” loan balances transitioned into severe delinquency at a 5.2 percent rate in the fourth quarter, also the highest since 2011. Nearly 2.7 percent of auto loan balances transitioned to delinquency in the fourth quarter, the highest since 2010.

Although outstanding credit balances are clearly high in nominal terms, they are not out of historical line when compared to metrics such as consumer spending or debt service-to-income ratios. Nonetheless, expectations for slower income growth in the year ahead, along with rising delinquencies in some loan types for younger and lower-income consumers suggests that consumer financial stress will remain elevated for much of 2024 before beginning to improve.

February 15th, 2024

Get The News You Need

Sign up for our daily newsletter to receive all the most important industry news and updates every weekday morning.

Recent Posts

- Defending Credit in Oregon

- THIS THURSDAY | AFSA Webinar | Why AI Implementations Fail, and How Asset Finance Lenders Can Get It Right

- Amendment to H.R. 8800

- On Brian Johnson’s Nomination to Lead the CFPB

- June White Paper | Consumer Complaints