Recent Fed Reports Point to Tighter Consumer Credit

Two reports released by the Federal Reserve in May show credit conditions are tightening across the economy.

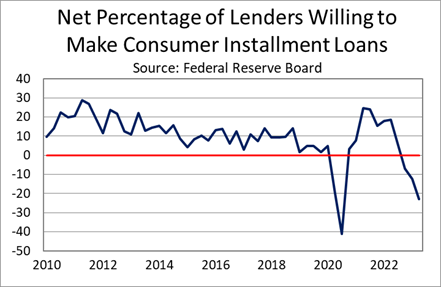

The Federal Reserve Board’s Senior Loan Officer Opinion Survey on Bank Lending Practices, provides information on bank credit availability, loan demand and lending practices for both commercial and household borrowers. The latest results from the survey conducted in late March and early April show that households faced tighter standards across all types of loans—credit-card, new and used auto, consumer installment and mortgages. Indeed, the net percentage of lenders tightening standards (e.g., lowering credit limits, raising minimum required credit scores, raising minimum repayments, and decreasing maximum maturity) was at its highest since 2020, amid high levels of pandemic uncertainty.

In fact, the net percentage of domestic lenders willing to make a consumer installment loan fell for the sixth quarter in a row, reaching -22.8. Only 1.8% of respondents were more willing to extend such a loan compared to three months earlier versus 24.6% who were less willing.

Although the survey does not distinguish between prime and subprime consumer loan borrowers, it found that the net percentage of lenders tightening subprime mortgage standards also increased to its highest since the second half of 2020. At the same time, household demand for each of the products fell, reflecting the impact of higher interest rates and reduced optimism for economic conditions.

The Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit for the first quarter, drawing on Equifax data, looks at the credit situation from the household perspective. Both mortgage and auto loan originations tumbled in the first quarter. And while aggregate delinquency rates remained significantly below levels reported immediately prior to the pandemic, signs of stress are emerging. Transition rates for credit cards, auto loans and mortgages into both delinquency and serious delinquency increased during the quarter.

More recent data compiled by Cox Automotive suggests these trends continued into the second quarter. According to Cox, “Access to auto credit tightened in April across all loan channels and lender types.” Meanwhile, auto loan performance is tracking below last year’s levels, but defaults remain well below historic trends.

June 2nd, 2023

Get The News You Need

Sign up for our daily newsletter to receive all the most important industry news and updates every weekday morning.

Recent Posts

- Consumer Confidence & Credit

- AFSA Webinar | Servicing Is Eating Originations: What Lenders Are Missing After the Loan Is Booked

- Industry Expertise | The Exposure Gap Your Bank Partnership Agreement Just Created

- AFSA Connects on the West Coast

- AFSA Testifies on Capitol Hill