Don’t Overplay Data or Underestimate Credit

There is plenty of bad economic news to go around: Inflation trends not seen in more than 40 years; 401(k)s and investment funds taking devastating hits seemingly every day; skyrocketing fuel prices and business costs; ongoing supply chain crises; and regulatory over-reach that may kneecap businesses and consumers alike. Reporters don’t need to be adding to what is already a compelling gloom and doom narrative with incomplete data and less than clear outcomes.

The latest example of this? The Wall Street Journal’s headline blares, “More Subprime Borrowers Are Missing Loan Payments” (May 19, 2022), but the story fails to add necessary context. It may be accurate that some lenders have seen an increase over the past financial quarter of subprime borrowers missing loan payments, but the bigger picture reveals a more complex story with some silver linings.

First, the slight increase quarter over quarter of missed payments is occurring in a time of the healthiest consumer lending environment on record in the U.S. The uptick in delinquencies is taking place after months of increases in savings rates and record low delinquencies. In short, delinquencies in some market areas may be returning to pre-pandemic norms when many areas of our national life are similarly returning to normal.

As the Journal notes: “Lenders say that delinquencies are going up from artificially low levels and that their credit portfolios overall remain strong. Many refer to what is happening as a normalization, where delinquency rates return to levels more in line with prepandemic times. Some say their delinquencies remain below their first-quarter 2020 levels.”

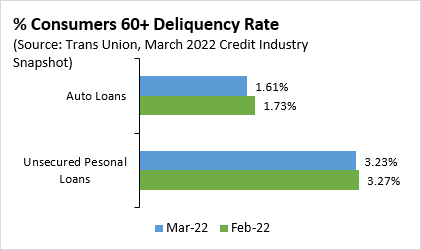

In fact, as AFSA chief economist Perc Pineda notes, “First-quarter data from the New York Fed shows the percentage of auto loan balances that were 90+ days delinquent decreased. TransUnion data similarly shows that the subprime auto 60+ delinquency rate decreased from 12.01% in February to 11.19% in March. Meanwhile, unsecured personal loan 60+ delinquency rate increased only negligibly from 13.89% in February to 13.95% in March.”

In fact, as AFSA chief economist Perc Pineda notes, “First-quarter data from the New York Fed shows the percentage of auto loan balances that were 90+ days delinquent decreased. TransUnion data similarly shows that the subprime auto 60+ delinquency rate decreased from 12.01% in February to 11.19% in March. Meanwhile, unsecured personal loan 60+ delinquency rate increased only negligibly from 13.89% in February to 13.95% in March.”

In total, Pineda adds, the percentage of consumer loans with a 60+ delinquency rate remains low and has decreased. With the economic growth slowing, it will impact consumer credits. But the latest data does not support claims of a serious deterioration of consumer credit in the near term.

Second, the article fails to note that historically, delinquencies rise in the 1st Quarter of the year. For example, some people may be prioritizing bill payments coming off increased spending at Christmas. However, delinquencies tend to drop again in the 2nd Quarter.

Third, while the article claims there is “broader concern among some lenders about the ability of consumers overall to keep up with payments” the quotes that follow contradict that thesis. A Wells Fargo representative notes that “we are still in the best credit environment;” a Capital One official says, “We would expect this is an across-the-board kind of return to normal over time.”

Fourth, the article undercuts its own message by burying a couple crucial points: fewer consumers are in subprime credit than pre-pandemic, indicating they have improved their credit standing. Many consumer lenders continue to see lower than normal delinquencies. And, as Fitch Ratings noted, some large card lenders didn’t record a delinquency increase year-over-year. This is good news, and points one might think important given the bad economic news of the day.

What does all this mean? A “Chicken Little / Sky-is-falling” headline does not a story make. The financial standing of U.S. consumers is in many ways stronger than it may have been 18 months ago, and what delinquencies may be occurring appear to be within well-accepted historical trends. That said, there are large swaths of consumer data that must be considered before any final judgment is rendered. Most importantly, while the media likes to over-estimate the dire straits of the economy, the crucial role of credit for all consumers should not be underestimated.

May 19th, 2022

Get The News You Need

Sign up for our daily newsletter to receive all the most important industry news and updates every weekday morning.

Recent Posts

- 🚨THIS THURSDAY | AFSA Webinar | Beyond the Paperwork: Stopping Asset Finance Fraud with Identity Intelligence and Intelligent Decisioning

- AFSA Shares Debt Collection Rules FAQs

- Chopra CFPB vs. Current Bureau

- Job Growth Slows

- July White Paper: Repossession Moratoria