New Data Reiterate Importance of Consumer Credit

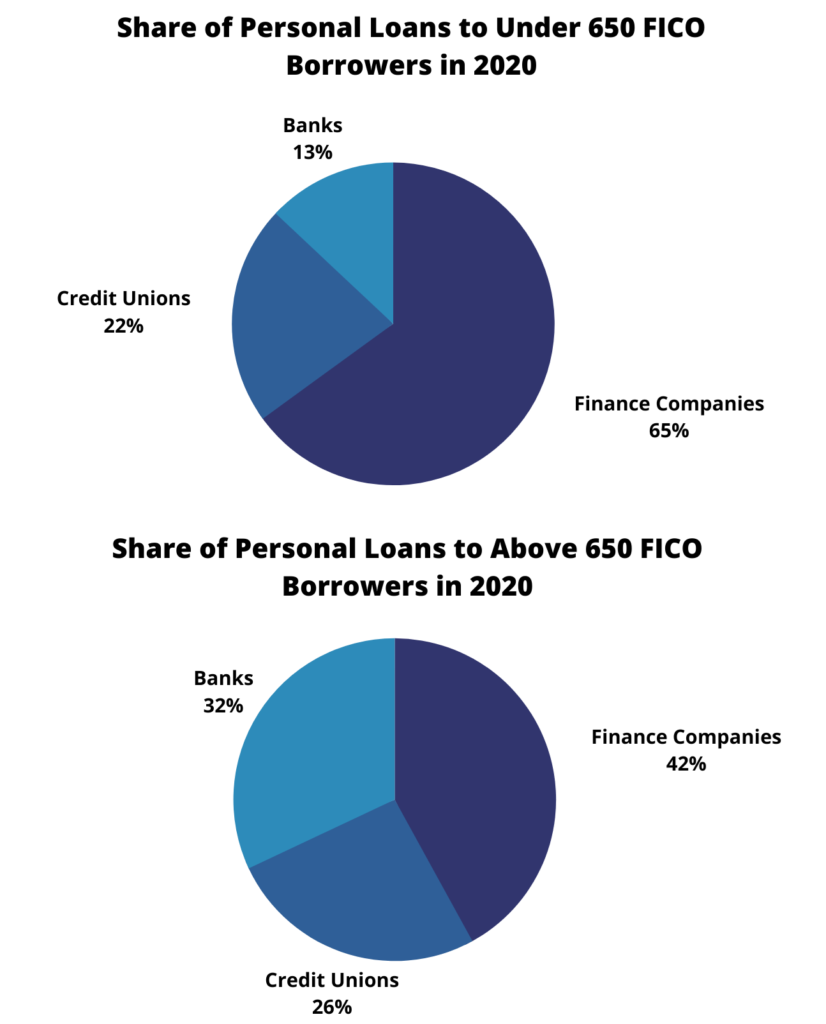

New data finds that 65 percent of personal loans to consumers with non-prime credit scores (less than 650 FICO score) in 2020 were made by consumer finance companies. This is more than double the number of loans issued to these borrowers by credit unions (22%) and traditional banks (13%). At the same time, banks and credit unions provided 58% of all personal loans to prime customers (above 650 FICO score) last year, while 42% of these customers choose a consumer finance company product.

Individuals with good credit scores have choices for credit needs. Conversely, nearly 1 in 3 U.S. consumers are considered subprime borrowers who may not have access to traditional banking services or credit cards.

Policymakers often buy-in to the inaccurate stereotypes of advocacy groups that target consumer finance companies as “predatory,” or misunderstand interest rates. As this new data shows, policies such as rate caps restricts credit to Americans who may need it most. Arbitrary rate caps and other laws that restrict access to credit redline credit for those with higher credit scores and cut off those who may have less than pristine credit or no access at all.

Access to credit should not be limited to those consumers with pristine credit, and subprime borrowers should not find themselves in a credit desert. Many financial service providers, such as state-licensed traditional installment lenders, continue to ensure millions of Americans, regardless of economic status, have access to safe and affordable products that meet their financial needs every day.

June 15th, 2021

Get The News You Need

Sign up for our daily newsletter to receive all the most important industry news and updates every weekday morning.

Recent Posts

- Industry Expertise | The Exposure Gap Your Bank Partnership Agreement Just Created

- AFSA Connects on the West Coast

- AFSA Testifies on Capitol Hill

- Colorado Automated Decision-Making Technology

- New Guidance on Non-Work Authorized Borrowers